The Universal Journal: Facilitating Continuous Accounting with One Source of the Truth

by Birgit Starmanns, Senior Director, Global Head of oCFO COE Thought Leadership Strategy and Programs, SAP

One of the key innovations introduced with SAP S/4HANA Finance is the Universal Journal. Many SAP customers have heard of it, but some are not quite sure exactly what it means. Simply put, the Universal Journal is a single table that contains both financial (FI) and controlling (CO) information as well as selected logistics and operational information, to enable, as it is popularly called, a “single source of truth.” This innovation makes the prior method of separate tables for the finance and controlling modules unnecessary.

And although the underlying table structure has changed from prior SAP ERP Central Component (SAP ECC) releases, it is important to realize that the workflows of transactional flows — including order-to-cash and procure-to-pay processes — have not changed. In addition, the logic of the postings – such as the accounts to which postings occur for a goods issue, for example — has also not changed.

Explore related questions

The learning objectives of this article include:

- Introducing the concept of continuous accounting, which is enabled by the Universal Journal

- Defining the Universal Journal, including the information that it contains across financial, controlling, and operational processes

- Illustrating the flexibility of the user interface and personalization available for each business user for information contained in the Universal Journal

- Exploring the migration paths available to move from SAP ECC to the Universal Journal in SAP S/4HANA Finance

To begin, let’s discuss the concept of continuous accounting.

What Is Continuous Accounting?

Continuous accounting refers to the idea of enabling real-time access to information at any time, not just after a period close. Prior to SAP S/4HANA Finance, a period-end close — be it a month-end, quarterly, or annual close — meant a series of batch processes that needed to be run overnight after the end of the period. In addition, if a process contained errors, those errors would need to be corrected and the batch process would need to be run again. Only then could follow-on, dependent processes continue.

With SAP S/4HANA Finance, supported by the Universal Journal, it is possible to access information at any point, without the need to wait for a period-end. Information is available in real time, and batch processes that formerly needed to run overnight can now run in seconds or minutes due to the in-memory architecture of SAP HANA.

As shown in Figure 1, it is now possible to always see the financial status of the company at any time, at any level — from the business unit to the legal entity to the group level to the corporate headquarters.

Figure 1 The concept of continuous accounting enables finance and risk teams to eliminate bottlenecks and guide the business at any time

With continuous accounting, the workload is distributed throughout the period. And with this real-time insight, finance teams can monitor issues in real time and take immediate action, not only until after month-end close. These teams can also now provide strategic insight to the business on forward-looking decisions with immediate access to information without the period-end bottlenecks, and without needing to wait until after a period close.

Now that we understand the vision and the benefits of continuous accounting, let’s look at what is meant by the Universal Journal, and how it is the key to enabling continuous accounting.

The Universal Journal — Defined

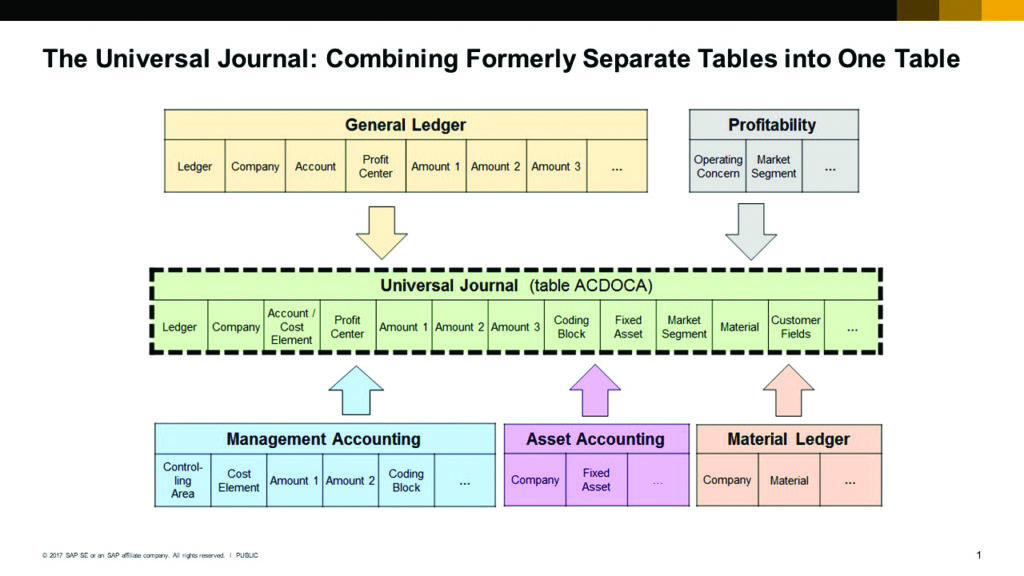

The Universal Journal is a single table, ACDOCA, that contains all financial, subledger, and controlling information. As shown in Figure 2, separate tables for finance information, including subledgers (such as accounts receivable, accounts payable, and asset management) and controlling processes (such as cost centers, projects, internal orders, profit centers, profitability analysis, and the material ledger) are no longer necessary.

Figure 2 The Universal Journal includes all the data fields that were previously stored in separate tables across financial, subledger, and controlling modules

As a special note, originally only the account-based profitability analysis (CO-PA) tables were incorporated into the Universal Journal, because the operating concern here was based on general ledger (G/L) accounts. In cost-based profitability analysis, the value fields were not mapped directly to G/L accounts. That being said, in a new scenario, mapping capabilities exist from cost-based CO-PA into the Universal Journal when using the Central Finance deployment option.

In addition, there are operational and logistics fields that are incorporated into the Universal Journal for better immediate analysis. Using accounts receivable as an example, prior to the Universal Journal, a report would indicate an issue with a specific receivables account. However, to see details about the profit center to which the transaction was posted, a controlling report needed to be accessed. And to see details about the customer and the product in question, additional operational reports were necessary, and so on.

Now, with the Universal Journal, all information is available based on one table and can be incorporated into one report. (Additional information about reporting is available in the next section, “Personalized Reporting Based on the Universal Journal.”)

From a technical standpoint, when leveraging the in-memory technology of SAP HANA, there is also no need for totals tables or index tables, since information can be calculated and aggregated only on the Universal Journal table entries very quickly. And without these additional index and totals tables, there is a reduced footprint required in the database, as well as an eliminated need for most reconciliations that occurred in the past that took place between transactional and totals tables.

Finally, the limitation of 999 line items in a journal entry is also eliminated; a journal entry can now (technically) have up to 999,999 line items, although such a business requirement is likely rare.

Now that we understand the Universal Journal, let’s examine how end users can benefit from access to its personalized reporting and analytics.

Personalized Reporting Based on the Universal Journal

Information is displayed from the Universal Journal in a more user-friendly way, with SAP Fiori as well as with SAP Analytics Cloud. Data for business users is readily accessible; of course, information is only shown to individual business users based on their roles and authorizations. Even though the information is now more visual, each user can still only see information that they have permission to see, such as specific cost centers or company codes.

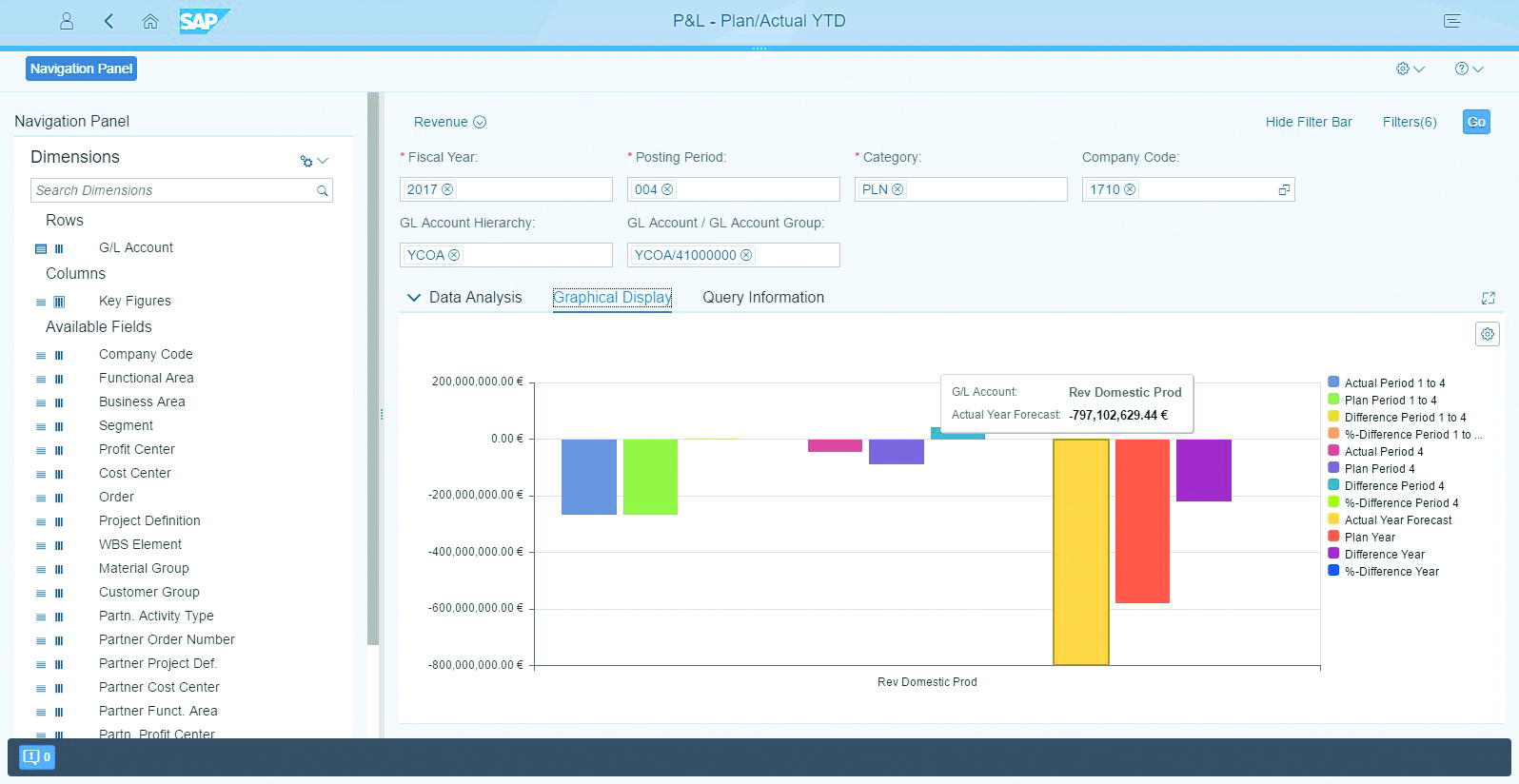

Information can be presented in a top-down view, for example through a calculation of key performance indicators (KPIs) such as days sales outstanding (DSOs), or an operating margin, based on the transactional information in the Universal Journal. In addition, summary information can be used to show comparisons, for example, a plan versus an actual budget report, based on the dimensions in the Universal Journal, as shown in Figure 3.

Figure 3 The dimensions available in the Universal Journal are shown in the left column, and can be used for further drill-down analysis

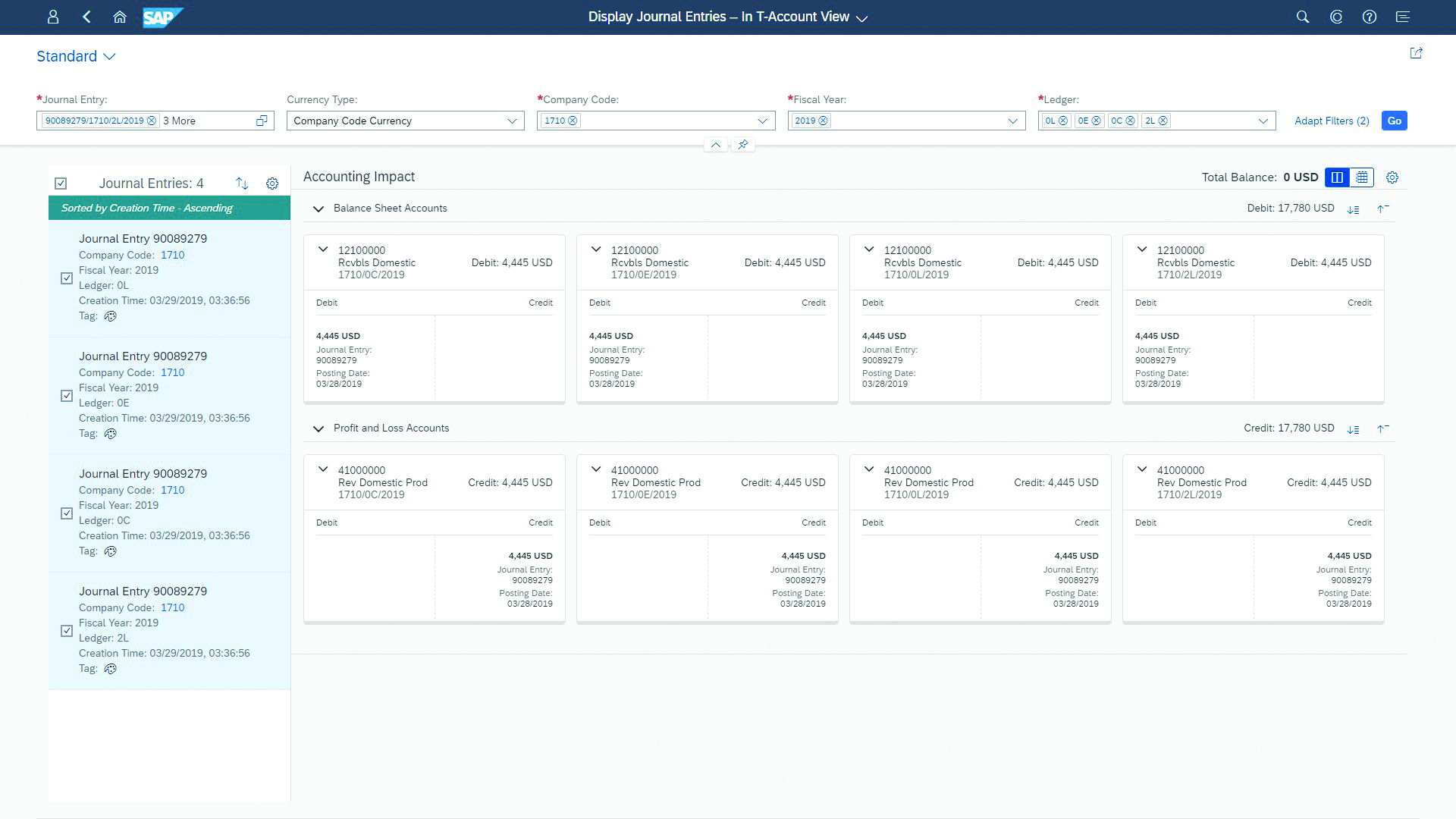

From a summary visualization, drill-down analysis to individual journal entries is possible. From this transactional perspective, in addition to displaying one journal entry at a time, new types of visualization are now possible — for example, a T-account view, which is a visual depiction of the postings to a G/L account (see Figure 4). Another option is showing a graphical representation of a document flow across operational and financial entries, such as a sales order to the goods issue to the accounts receivable documents, where drill-down access to the related Universal Journal transaction is available.

Figure 4 A T-account summary view shows debits and credits and the financial statement to which they were posted

Another example is a personalized drill-down analysis from the summary level. Some business users may want to sort by customer first and product second, others by profit center then the product, still others by geography first. For geography-based drill-down analysis, a map-based visual can be used to graphically show locations, along with an alert of potential issues based on personalized tolerance levels, such as a high percentage-based decline in sales.

Again, in each of these instances, only one journal entry is shown, since the Universal Journal contains all financial and controlling information in the same journal entry. No separate documents need to be created for the G/L account, for the cost center, for the profit center, and so on; all these dimensions are available in the one journal entry posted to the Universal Journal.

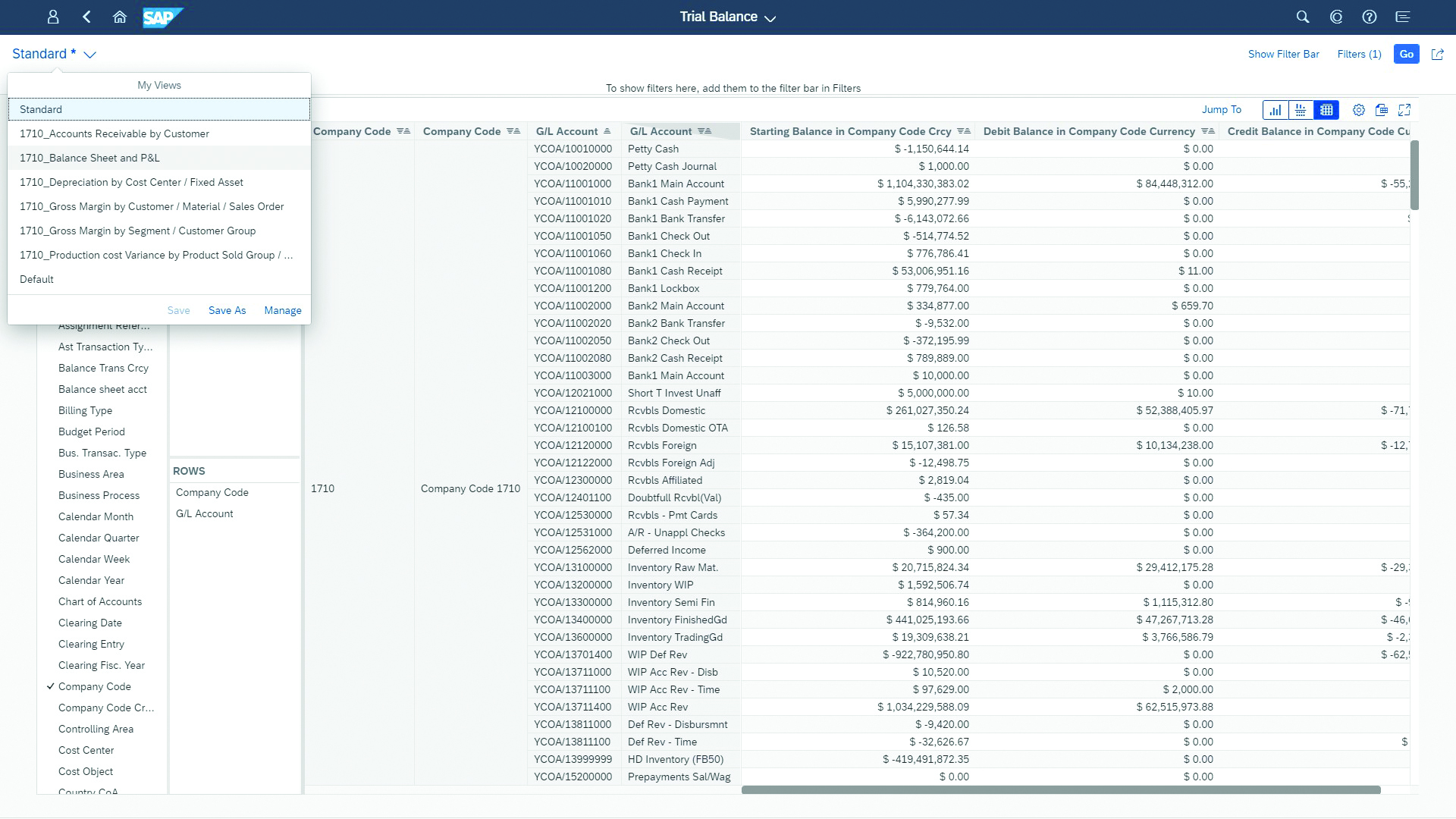

Of course, tabular views are still important to finance business users, for example, when it comes to trial balances of financial statements. In this case, business users can define their own views, as shown in Figure 5, without needing to go through IT to create report variants. As an example, in accounts receivable, knowing a customer is important, while the important data field for accounts payable is the vendor. Here, business users looking at a G/L account can determine which fields are required and use them to create their own views. As an additional benefit, IT is not encumbered by requests for often very similar views, and business users can see their results more rapidly.

Figure 5 A tabular view is still available, where business users can create their own views with the dimensions in the Universal Journal

With the real-time access due to in-memory technology capabilities, the Universal Journal now becomes one source of truth for both transactional processes and for analytics, and ultimately for planning. Plus, this data can be used to feed predictive scenarios.

Finally, let’s look at the G/L scenarios that were available in SAP ECC releases and how customers can move to the Universal Journal in SAP S/4HANA Finance.

Considerations for Migrating to the Universal Journal

For customers that are newly implementing SAP S/4HANA Finance, the Universal Journal is the only option, as it is the core finance and controlling table.

Customers that have implemented SAP ECC systems are required to move from their existing G/L to the Universal Journal in a move to SAP S/4HANA Finance. The first thing to keep in mind is that when moving from SAP ECC to SAP S/4HANA Finance, the Universal Journal is mandatory. It is the table structure for capturing transactions and making them available for further processing, as well as for analytics. It is not an option for customers to remain on the prior tables.

Existing customers run one of two scenarios:

- The classic G/L: This is the original G/L that was delivered with SAP ECC.

- SAP General Ledger: This G/L is often referred to as the “new G/L.” SAP General Ledger was provided in release 4.5 (which was renamed SAP ECC 5.0) using enhancement packages, and then made generally available in release 4.6 (which was renamed SAP ECC 6.0).

What Is SAP General Ledger?

SAP General Ledger offers more advanced capabilities than the classic ledger, including:

- Parallel ledgers, which support multiple accounting standards, for example, International Financial Reporting Standards (IFRS) as well as country-specific Generally Accepted Accounting Principles (GAAP) for financial reporting

- Standard reporting for these parallel ledgers in SAP General Ledger — while in the classic ledger, parallel accounting and reporting could only be accomplished using the special purpose ledger

- Online document splitting in SAP General Ledger, which enables the creation of financial statements such as balance sheets and income statements for business/market segment reporting, not just at the legal entity (company code) level

- Real-time integration between the FI and CO functionality for postings that occur across company codes, functional areas, and business areas

Scenarios for Migrating to the Universal Journal

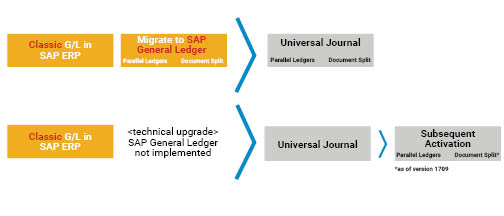

The primary question from customers is whether it is a requirement to first move to SAP General Ledger. The short answer to the question is — no, it is not required. There are migration scenarios available from either the classic G/L or from SAP General Ledger. However, the long answer is: if migrating from the classic G/L, there is a technical upgrade to SAP General Ledger that takes place automatically as part of the migration. That does not mean that there needs to be a full-scale functional implementation of SAP General Ledger; it simply means the table structures are migrated in the background. However, it is not necessary to activate SAP General Ledger functionality that was described above. These capabilities can be activated at a later time, as of release SAP S/4HANA Finance 1709 (see Figure 6).

Figure 6 Migration to the Universal Journal is available from both the classic G/L and SAP General Ledger

As a special case, to support multiple financial ledgers, many companies used special purpose ledgers while on the classic G/L to facilitate parallel ledgers if they had not yet implemented SAP General Ledger. With each special purpose ledger, new tables were created, meaning that reporting needed to be created from scratch. Since each special purpose ledger is defined uniquely by each customer, there is no migration path, and these parallel ledgers need to be configured in SAP S/4HANA Finance.

The good news is that once the ledgers are defined in the Universal Journal, standard reporting is available so that the reports do not need to be recreated.

Benefits Summary of the Universal Journal

As we have seen, the Universal Journal is the new underlying table structure for SAP S/4HANA Finance, with a migration path from both the classic ledger and SAP General Ledger. The benefits of the Universal Journal include:

- Use of the same source of data for transactions, analytics, and planning

- Incorporation of finance, controlling, and operational information in one source of the truth, drastically reducing the need for reconciliation between tables

- No change in the existing logic of financial postings

- A reduced technical footprint due to the elimination of the totals and index tables

- Ability for business users to define their own views without the need for IT intervention or the creation of redundant reporting variants

- Enablement of continuous accounting without the need to wait for batch jobs at period-end, for a reduction in bottlenecks, and an increase in real-time insights to drive strategic decisions

For more information about SAP S/4HANA Finance, including customer stories, please visit www.sap.com/finance.

Birgit Starmanns is the Global Head of oCFO COE Thought Leadership Strategy and Programs in the Global Center of Excellence for Finance and Risk. She also has responsibility for the go-to-market of new finance and risk solutions that leverage new technologies such as machine learning and cloud, and the business benefits they can bring to organizations. Her functional experience is in finance and management accounting, including SAP S/4HANA Finance, as well as core SAP ERP and SAP EPM. Birgit has over 30 years of experience across the Center of Excellence (COE), solution marketing, solution management, strategic customer communities and management consulting organizations. Prior to SAP, she was a principal in management consulting organizations, including Price Waterhouse and several boutique firms. Birgit holds a BA and MBA from the College of William and Mary.