Make-to-Order Manufacturing Planning Strategy with Planned Cost

How to Manage Planned Changes with Accurate Inventory Value On Books

by Venkata Ramana Nethi CSCP, CPIM.; Business Process Lead – Operations, Schlumberger

Organizations often experience challenges in a make-to-order (MTO) environment when managing “planned customer changes” mapping to standard product structure. This article will teach you how to separate “planned” vs. “un-planned” changes integrating planning, shop floor execution, inventory management and finance/controlling with accurate value on the books. It will explain inventory valuation with a step by step process for creating new custom MTO planning strategy configurations, implementing methodology, and interpreting the results. Learn how business can effectively manage MTO processes and avoid workarounds on month-end closing.

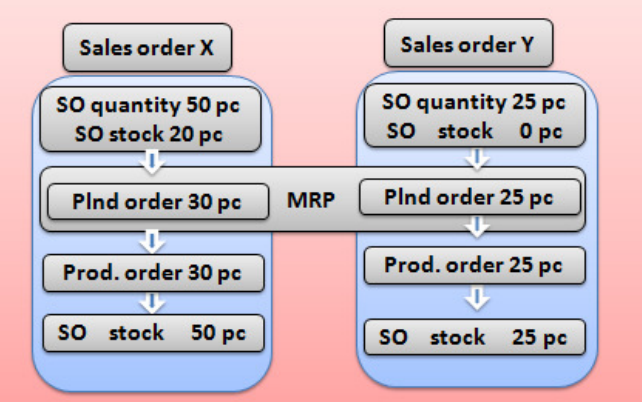

Make-to-order (MTO) is a business production strategy that is used due to product uniqueness or erratic demand. It allows a company to build a product after it has received a sales order and customize the product to the customer’s requirements. When working with MTO strategies, the sales order is the only pegged requirement. In an MTO environment, the net requirements calculation is carried out individually for every individual sales order. It is assumed that stock cannot be interchanged between sales orders. All procurement elements that are planned are created with direct reference to the sales order line item and are managed in the individual customer segment.

Explore related questions

It is commonly described as production and procurement based on it individual sales order line item rather than group requirements emanating from multiple demand sources. This direct reference to the sales order is also maintained down to the resulting production orders (Figure 1).

Figure 1: MTO Typical Scenario

SAP Planning Strategy 20

MTO strategy typically allows customer changes in both pull type and configurable manufacturing processes. This strategy has control over the allocated inventory pegged to sales order lines, so the production planner can review production order routing operations and components to meet customer specific requirements before releasing the orders to the shop floor.

During this process, specific production orders need updates on the component list (as per customer requirements) or the standard hours (due to shop floor conditions) of one or more operations in the production orders. Standard SAP planning strategy 20 allows you to produce a product or material to a sales order line.

However, in the real world the modified or updated components and routing operations become the base line planned cost to produce and deliver into the stock and the updates should not be considered as variances as the modifications will be charged back to the customer via sales order pricing strategies.

One limitation of standard planning strategy 20 is that it always compares to the material master’s standard cost for inventory value and variances on production order, it does not allow use planned cost in ‘Goods Receipt’ of production order header material, resulting in variances even though it is not the case. Planners/shop supervisors always need to explain the variances to the finance/controlling department during variances and settlement of the production order.

This results in month-end issues in most medium- to large-sized organizations.

Business Challenges with SAP Standard Planning Strategy 20

Product mix with make-to-stock (MTS) and MTO: When the organization has a mix of both MTS and MTO products, then a different approach is taken for MTS and MTO materials on month-end process.

Execution: Planned changes of the production orders are projected as variances and the inventory value is listed as the same for all production orders in SAP standard planning strategy 20, which is not the case in manufacturing processes where each order is unique to customer requirements.

Controlling: Finance and controlling teams need to settle sales order line, instead of following the same process of WIP, variance and settlement process like MTS products.

If a material is set up with standard SAP planning strategy 20, in reality each production order has a separate planned cost after updating the component or routing information on individual production orders, goods issues and operations will be confirmed and tracked during the manufacturing process and when the goods receipt is completed; then value of the goods receipt quantity will be maintained against the material master standard cost instead of the planned cost of the production order. When SAP standard planning strategy 20 is used then goods receipt inventory value is at standard cost, which is not the realistic situation.

Understand Standard Cost vs. Planned Cost

It is very important do understand the terminology of costs used on production orders especially in make to order environments.

Definition of Standard Cost:

- In MTS production, the target cost is the standard Cost.

- Standard cost – Every sales order item is valuated at the existing standard cost. The standard cost is the estimated cost for the production of a finish product based upon the standard conditions of production as of January 1

Definition of Planned Cost:

- In MTO production the target cost is the planned cost.

- Planned costs – Individual plan cost is calculated for every sales order item based on the production order for that sales order item using the order specific master data and the item is valuated at this plan cost from inventory valuation point of view.

If your organization allows workarounds to manage MTO production orders, answering the following questions will place you on the right path to explore how to resolve these challenges:

- Is there a way my goods receipt (101 Movement type) from a production order has a planned cost (real value instead standard cost from material master costing tab) of the production order?

- How can finance and materials management teams know the real value of the inventory on books when goods receipt occurred via production order goods receipt?

- Is there a way that can I manage MTO production order settlement like MTS production orders?

- Can I calculate variance (unplanned changes) against the production order planned cost instead of the material master standard cost?

- Can I avoid the sales order line controlling and leverage best practices of month end settlement on WIP, variance and settlement process?

If the answer to all above is YES, the MTO planning strategy described in this article is the approach to take.

This solution is applicable to both mid- and large-size manufacturing organizations using SAP ERP Central Component (ECC) as their ERP system.

The following sections demonstrate how a business can efficiently manage MTO processing and resolve the above-mentioned challenges integrating sales, manufacturing, inventory and controlling.

Configuration of New MTO Planning Strategy

In this section we’re going to configure a new MTO planning strategy called “Z9”. I will explain the reason behind the values by comparing to standard planning strategy 20 so that you understand the behavior during execution and review of the results.

Define Requirement Class

The purpose of this activity is to define requirement class, with which you control all functions relevant to requirements in logistics.

Notes: The requirement class controls the material requirements planning (MRP) and the requirements consumption strategy as well as the relevancy for planning. Specifications on the settlement of the requirement class, for example, the settlement profile and the results analysis key, are preferably used by materials management and do not have to be used when configuring the availability check and transfer of requirements.

Allocate a requirements class to the requirements type in next step.

This involved configuration in sales and distribution menu & controlling menu.

Create requirement class in sales and distribution menu (Table 1).

Table 1: Create Requirement Class in Sales and Distribution Menu

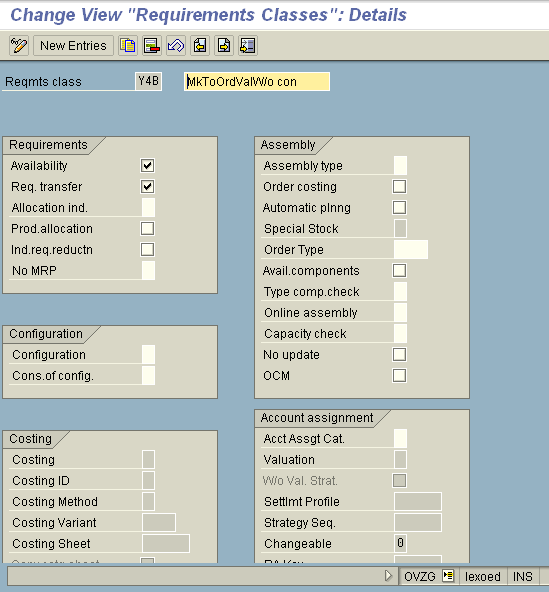

Step 1: Click New Entries and create requirement class (Figure 2).

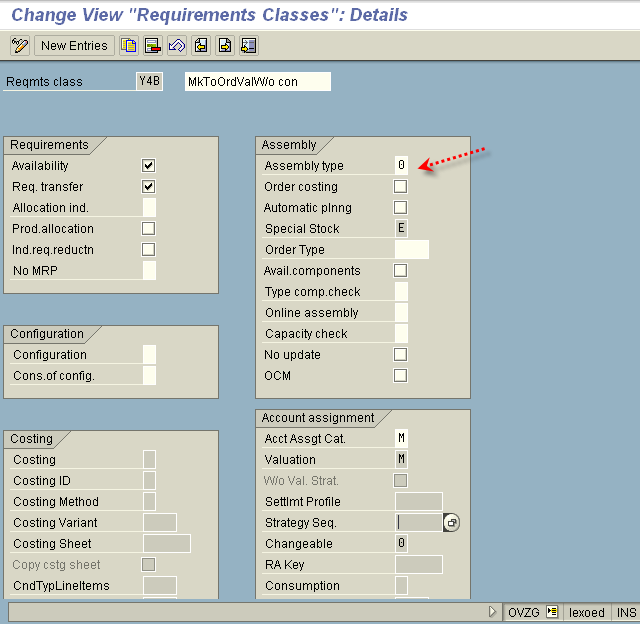

Figure 2: Transaction OVZG–Requirements Classes Configuration

Assign account & valuation in controlling menu (Table 2).

Table 2: Assign Account & Valuation in Controlling Menu

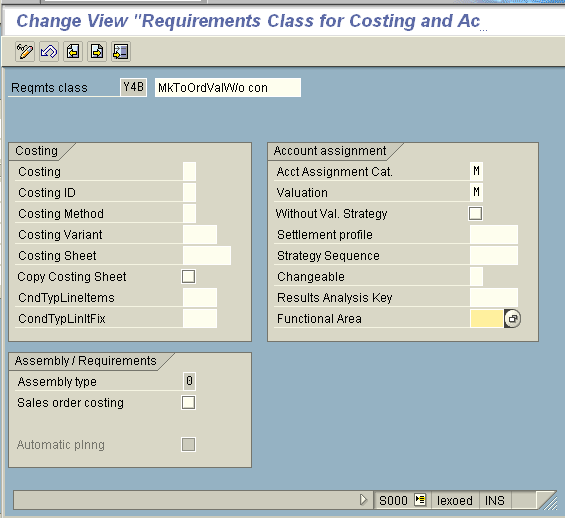

Step 1: Double click on Requirement class Y4B and maintain Account Assignment Cat as M and Valuation as M as shown in Figure 3.

Step 2: Save your entries.

Figure 3: Requirements Class Costing and Accounting

Assign account & valuation in controlling menu (Table 3).

Table 3: Assign Account & Valuation in Controlling Menu

Step 1: Double click on requirement class Y4B and maintain account assignment cat as “M” and valuation as “M.”

Step 2: Save your entries.

Assign assembly processing in sales menu (Table 4).

Table 4: Assign Assembly Processing in Sales Menu

Step 1: Double click on requirement class Y4B and maintain assembly processing as “0” (Figure 4).

Figure 4: Requirements Classes Assembly Processing 0

Let’s understand what’s in the custom requirement class settings comparing to the standard delivered.

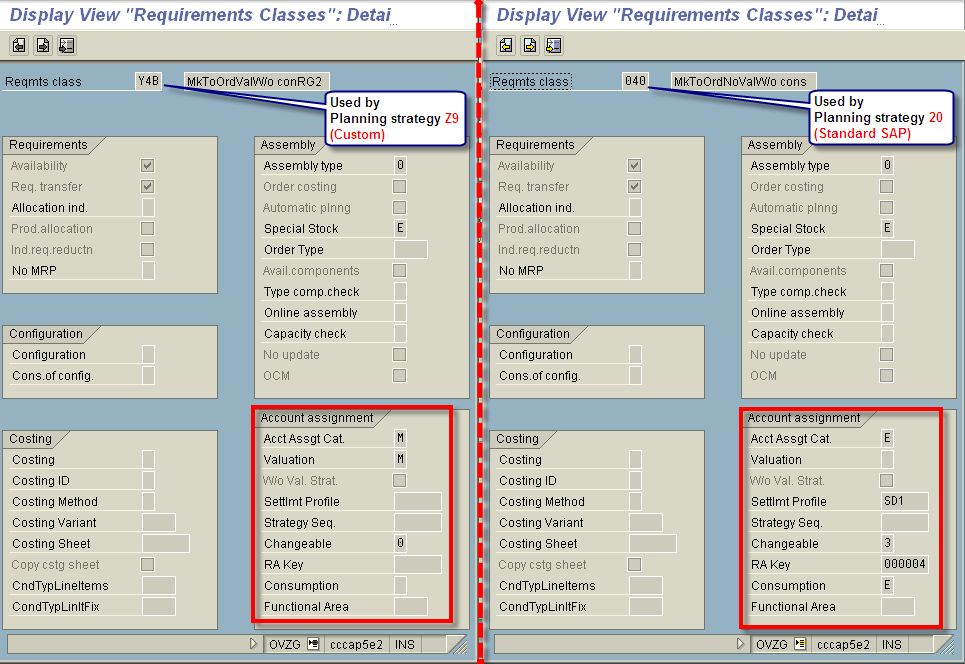

Figure 5 shows a comparison between the standard requirement class 040 used in standard planning strategy 20 and custom requirement class Y4B in custom planning strategy Z9.

Note:

- Custom naming convention should be as per your organization standards.

- Involve your Controlling team as this needs their review during settlement and valuation policies

Figure 5: Requirement Classes Comparison — Standard Vs. Custom (in this article)

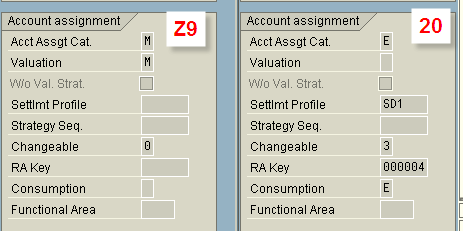

Let’s take a closer look at the significance of the ‘Acct Assgt Cat.’ and ‘Valuation’ between standard planning strategy 20 and the custom planning strategy Z9 mentioned in this article (Figure 6).

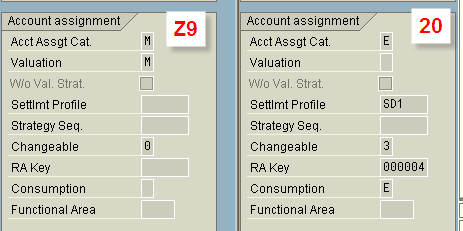

The account assignment category determines which account assignment data (such as cost center, account number, and so on) is necessary for the item.

M Ind. cust. w/o KD-CO E Ind. cust. w. KD-CO

Figure 6: Acct Assignment Category—Standard Planning Strategy 20 vs. Custom Planning Strategy Z9

Differences between M and E is consumption posting

- M = Opposite of E

- E = Sales order item as cost- and revenue-carrying

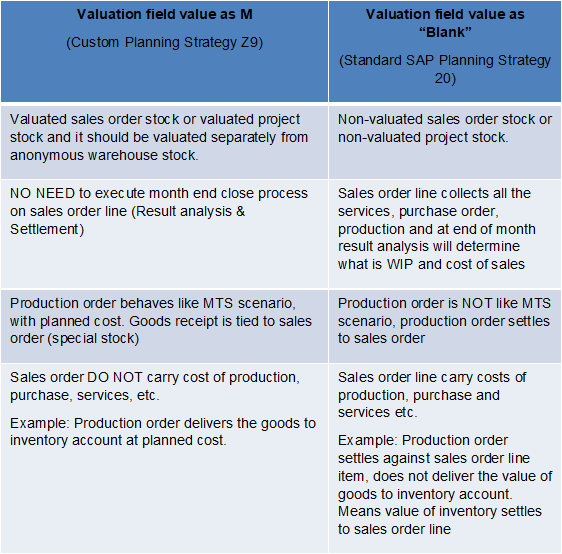

Valuation of Special Stock (Definition)

Determines whether sales order stock or project stock is managed on a valuated or non-valuated basis.

Use:

- If you use valuated sales order stock or valuated project stock, the quantity and value flow is the same as that of anonymous MTS production.

- If you use non-valuated sales order stock or non-valuated project stock, you must carry out a results analysis in the course of period closing if you want to determine the stock values of finished and unfinished products.

Understanding the significance of ‘Valuation’ between standard planning strategy 20 and the custom planning strategy Z9 mentioned in this article (Figure 7).

M – Separate Valuation with reference to sales order

Blank – No Stock Valuation

Figure 7: Valuation Comparison in Requirement Class Configuration

Deep Dive into the Behavior of ‘Valuation’ Between M and ‘Blank’ (Table 5).

Table 5: Behavior of Valuation Between ‘M’ and ‘Blank’

This concludes the detailed explanation of Requirement Class.

Define Requirement Type

Now we continue next steps of the configuration, which are further required steps to complete the configuration.

Procedure (Table 6).

Table 6: Procedure for Configuration

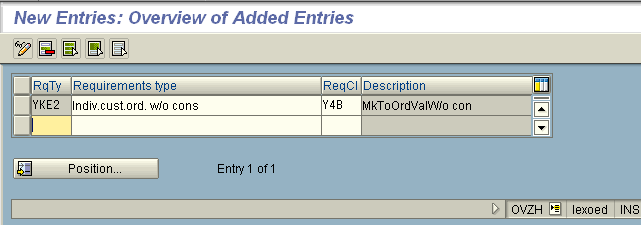

Step 1: Create a new entry for Requirement type ‘YKE2’ and assign Requirement class ‘Y4B’ (Figure 8).

Step 2: Save your entries.

Figure 8: Transaction OVZH—Requirement Type Configuration

Define Planning Strategy

The planning strategy represents an appropriate procedure to be used for planning and produced a material.

Procedure (Table 7).

Table 7: Procedure for Planning Strategy

Step 1: Click New Entries.

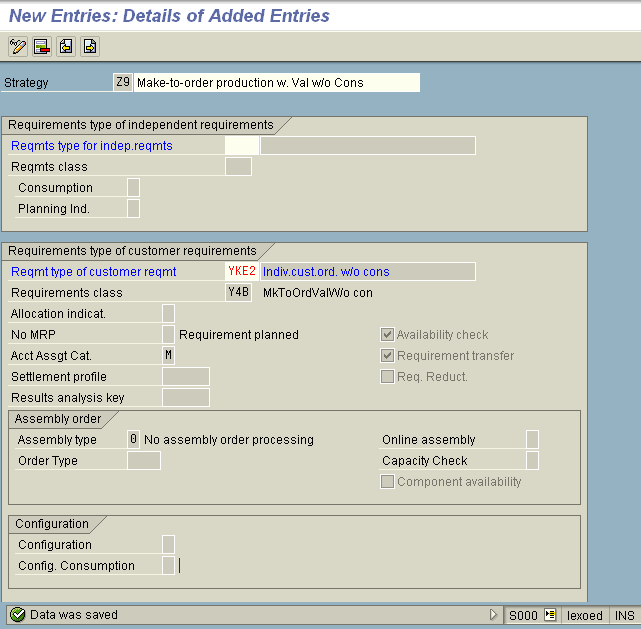

Step 2: Create a new planning strategy “Z9”” and assign requirement type YKE2 in Requirements type for customer requirements section (Figure 9).

Step 3: Save your entries.

Figure 9: Transaction OPPS—Planning Strategy Z9 Customer Requirements

Define Strategy Group

In this step, you group strategies together into a strategy group. You can allocate the strategy groups to the materials directly in the material master record

Procedure (Table 8).

Table 8: Procedure for Defining Strategy Group

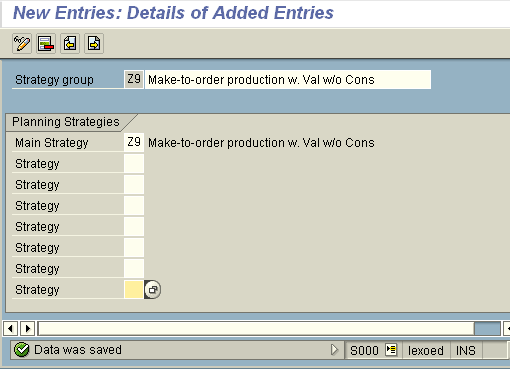

Step 1: Click New Entries.

Step 2: Create planning strategy group “Z9” and assign planning strategy Z9 as Main Strategy (Figure 10).

Step 3: Save your entries.

Figure 10: Transaction OPPT : Planning Strategy Z9 as Main Strategy

Result Review: New MTO Planning Strategy Z9 is ready for use on material master

Configuration of Production Order Type Dependent Parameters

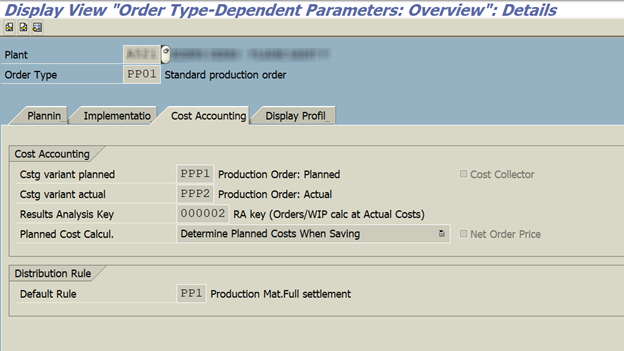

In this configuration of production “Order Type-Dependent Parameters” we will review cost accounting tab only which influence production order costing. You must review other tabs as per your business requirements.

Note: Coordinate with your plant controller as this drives redetermination of planned cost on production order planned updates and month-end settlement process. Transaction OPL8 (Order type dependent Parameters), use below settings as shown in Figure 11.

Figure 11: Transaction OPL8—Order Type Dependent Parameters, Cost Accounting Tab

Master Data: Assign the New Planning Strategy to Material Master

Assign this planning strategy material master on MRP view using MM02 transaction and maintain individual/collective requirements value as per your product structure.

Additional Notes:

Influencing MTO at the Component Level The individual/collective indicator in the material master record determines whether a component is procured for a special customer requirement in the individual segment.

- The indicator “1” – means that the material is being specially manufactured or procured for a sales order.

- The indicator “2” – means that the material is manufactured or procured for various requirements.

- The indicator “ ” – means that the material should be planned the same way as the immediate parent requirement.

Execution Scenario

- Review Cost estimate: MM02 and CK13

- Review Sales order Demand: MD04

- Run MRP: MD02

- Create two production orders with different planned cost

- Goods receipt: MIGO

- Review Results: MB51

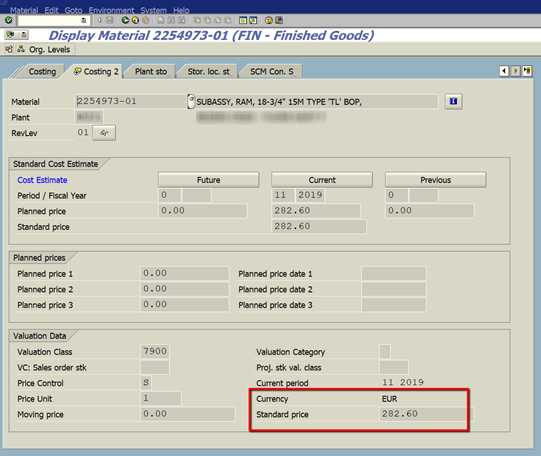

Standard Cost: The BOM (Bills of Material) and Routing (master list of operations to perform insequence) is used to roll up the cost of the product, which is maintained as ‘Standard Cost’ on Costing view of material master’s “Costing 2” tab as shown in Figure 12.

Figure 12: Transaction MM03—Review Costing 2 Tab

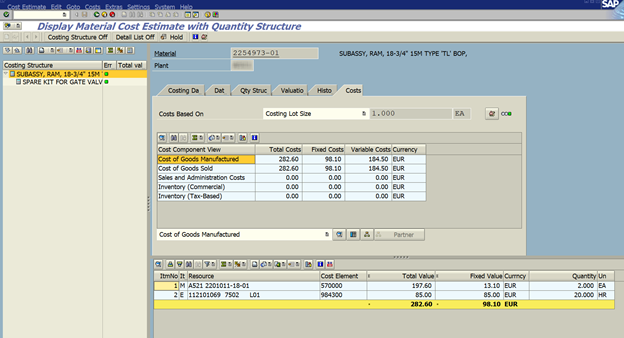

Display cost estimate via CK13 Transaction, as shown in Figure 13.

Figure 13: Transaction CK13—Cost Estimate Display

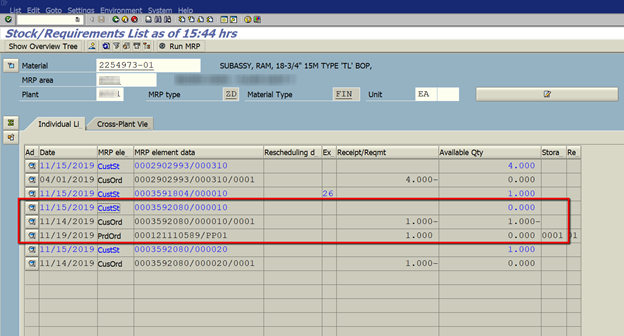

In the MTO scenario, demand and supply are uniquely identified with hard pegging sales order line. On the stock requirements list (Transaction MD04) Sales Order 0003592080/000010/0001 exists, run MRP to generate planned order and convert into production order 000121110589/PP01, as shown in Figure 14.

Figure 14: Transaction MD04—Stock Requirements List

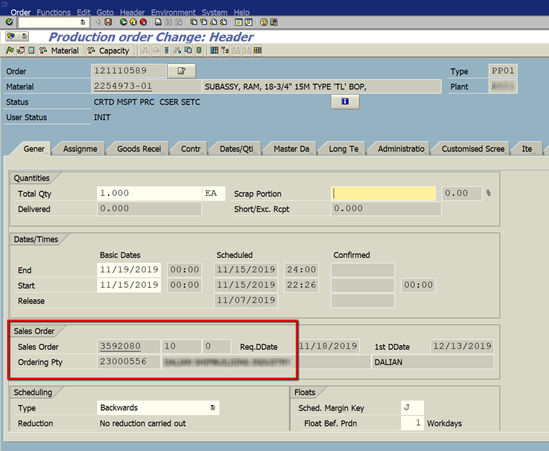

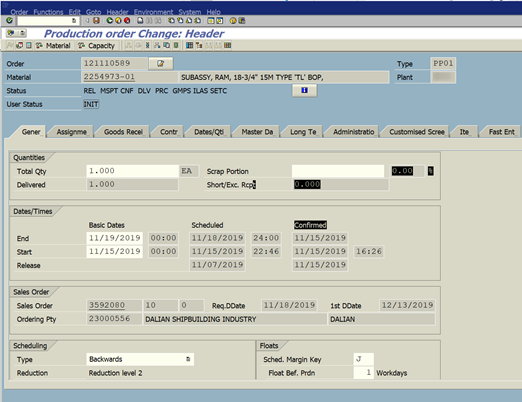

You can see that the Production order 121110589 is pegged to Sales Order 3592080/10, via Transaction CO02, as shown in Figure 15.

Figure 15: Transaction CO02—Production Order

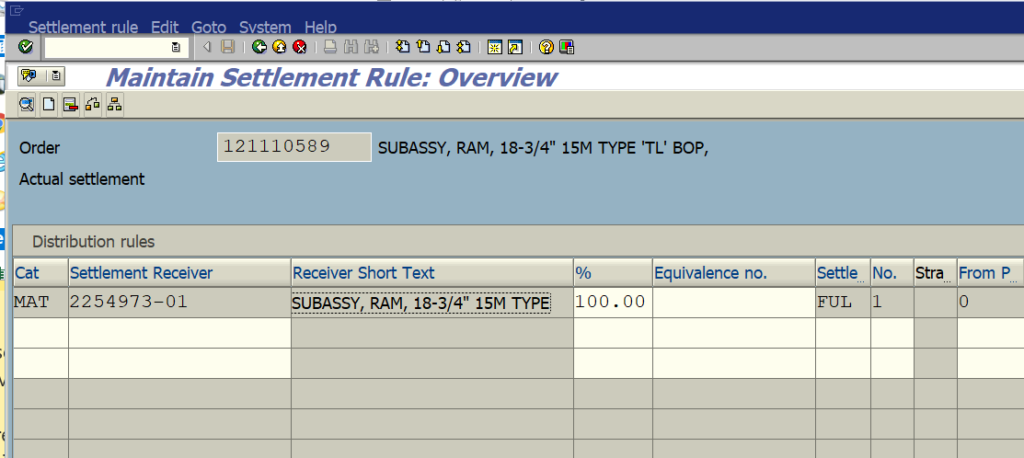

Settlement receiver is Material, via transaction CO02’s menu Header> Settlement Rule, as show in below Figure 16.

Figure 16: Transaction CO02—Settlement Rule

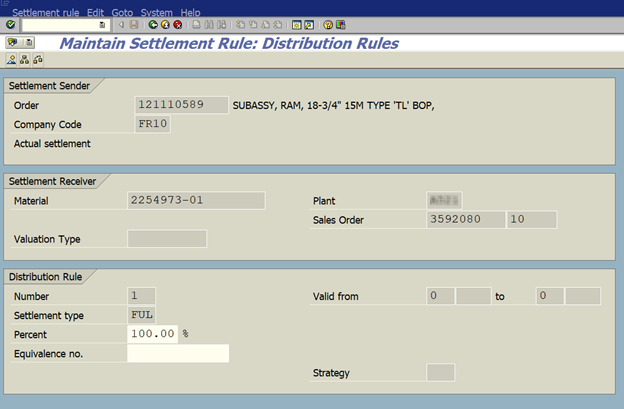

Category ‘MAT’ carry the Distribution rules and Settlement receiver is Material, with Sales Order pegging, as shown in below Figure 17.

Figure 17: Transaction CO02—Settlement and Distribution Rules with Sales Order

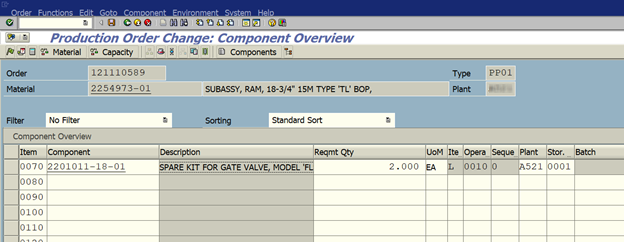

When the planner creates production order from MRP generated planned order the component quantity and operations are as per Bills of Material and Routing. Figure 18 shows the production order component qty as 2 as per BOM.

Note: We will change the component quantity to showcase the planned changes in next step and review how the planned cost is updated.

Figure 18: Transaction CO02—Production Order Component Overview

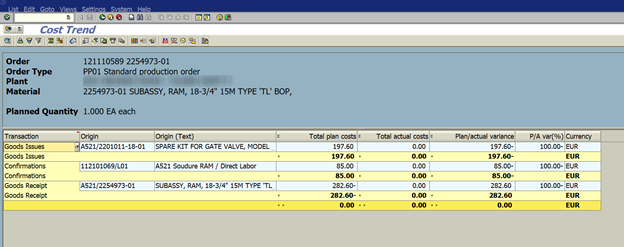

Let us review the cost analysis of Production order via CO02 menu Goto > Cost Analysis, the planned cost of Goods Issues (input components), Confirmations(operations) and Goods Receipt (Header Material) match today standard cost estimate as shown in below Figure 19.

Figure 19: Transaction CO02—Cost Analysis

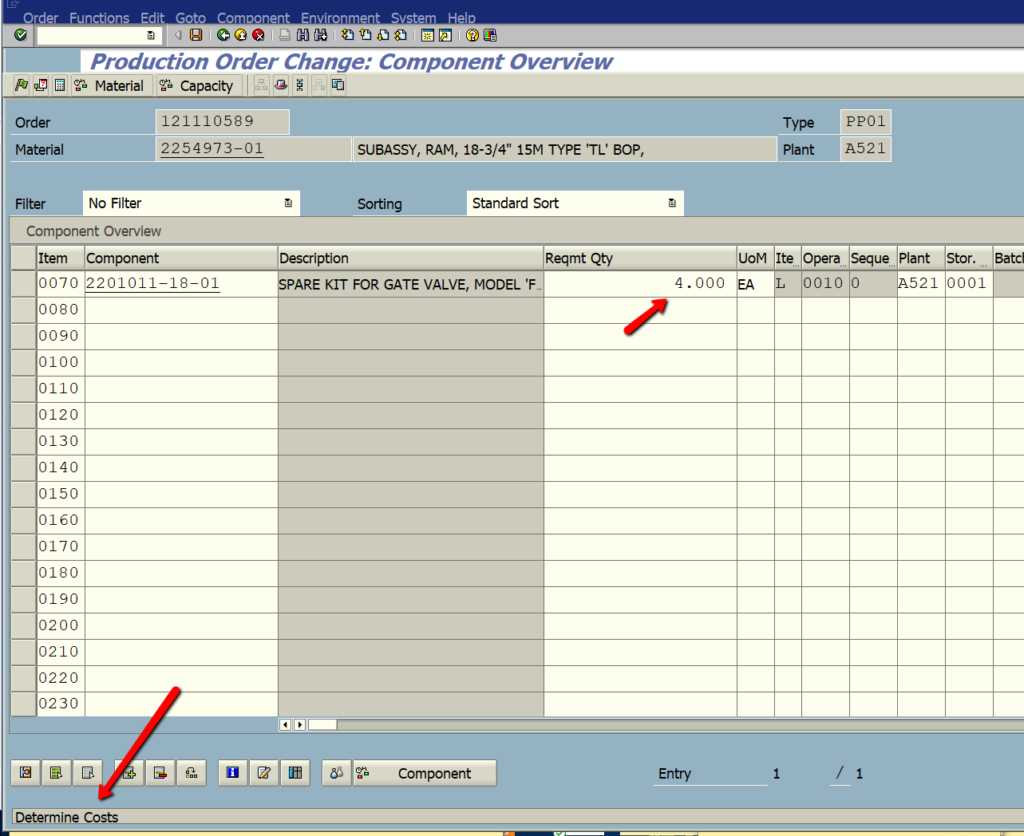

In our business scenario the planner or shop supervisor reviews customer specific requirements and updates the production order component qty before releasing to shop floor for execution. To showcase the behavior of the new custom planning strategy the component quantity is being increased from 2 EA to 4 EA (means the cost of components is twice than original).

What is Expected?

Additional component quantity (modified is planned change) is used to update the planned goods receipt value of the product. Which should reflect during material movements and posting value on books. The production order component quantity is increased from 2 to 4, as shown in Figure 20.

Note: This is an example so component qty is changed, however you can add additional materials or delete from the list are possible scenarios and all are supported. When you SAVE the production order, the planned cost is re-determined based on the OPL8 Configuration mentioned in Figure 11.

Figure 20: Transaction CO02—Production Order Component Overview

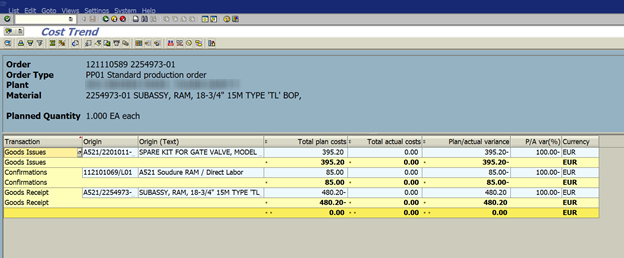

Let’s see the revised updated Cost Analysis with the planned changes performed in above step from Menu of CO02, Goto>Cost Analysis as shown in Figure 21.

Here is the interesting observation when the input Goods Issues cost increased and the Goods Receipt value is redetermined accordingly, as shown in Figure 21.

Figure 21: Transaction CO02—Cost Analysis After Component Qty Changed From 2 to 4 EA

Now the execution of production order follows by goods issue (MIGO) and Confirmations (CO11n or via MES systems).

Note:

- In this example Warehouse transitions included but not explained in detail as those are specific to your customizations; also, here the confirmation is at operation level. It can be a case to perform at header level based on your manufacturing process.

- Depending on the product, the complexity of the Bills of Material and Routing operations vary from few to hundreds in counts.

Actions completed:

- Good Issue Completed via MIGO

- Confirmations Completed via CO11n

- Goods Receipt Completed via MIGO

Review Results and Benefits

To focus on the objective, let’s review the production order delivery, material documents, and cost analysis after both Goods issue and confirmations complete.

Production order status updated with DLV (Delivered) can be reviewed via Transaction CO02 as shown below (Figure 22).

Figure 22: Transaction CO02—Production Order Status as DLV

Let’s see the benefits for the manufacturing team, materials, finance and controlling business teams and how updated planned cost is effectively managed avoiding workarounds on month end closing.

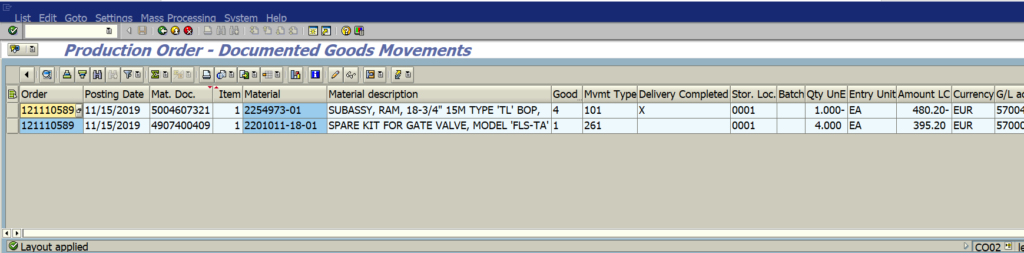

Using Transaction CO02 you can review the Documented goods movement which shows the material documents posted via MIGO, as shown below in Figure 23.

Figure 23: Transaction CO02—Documented Goods Movements

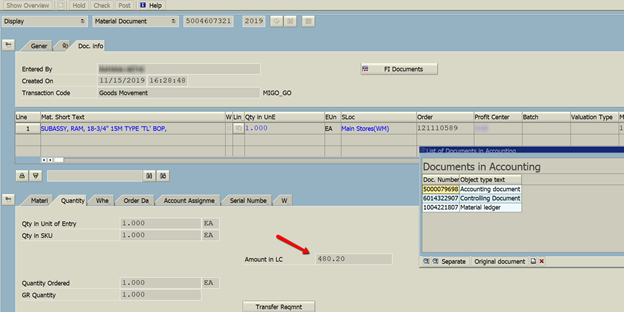

On the goods receipt material document the value is the redetermined (new) planned cost of the production order instead of standard cost from material master as shown below (Figure 24).

Benefit: Every production order is unique in nature, so the planned goods receipt is from the order.

Figure 24: Transaction MB51—Goods Receipt Material Document

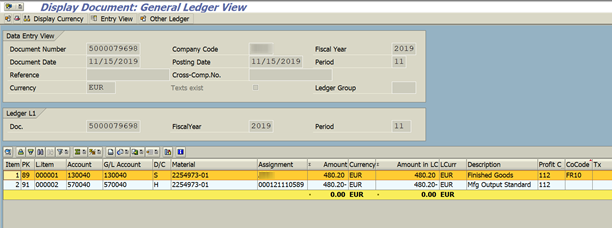

Accounting Document has the updated planned cost. You can review via transaction FB03 or you can navigate via Material doc as shown below in Figure 25.

Figure 25: Transaction FB03—Accounting Document via Material

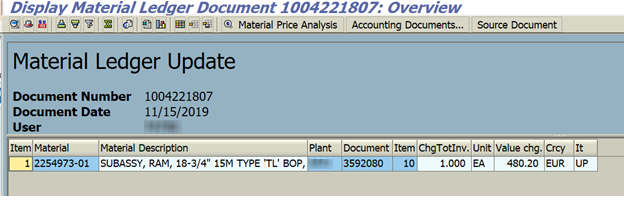

Material Ledger Update can be reviewed via Transaction CKMB or you can navigate via Material doc. as shown in Figure 26.

Figure 26: Material Ledger Update

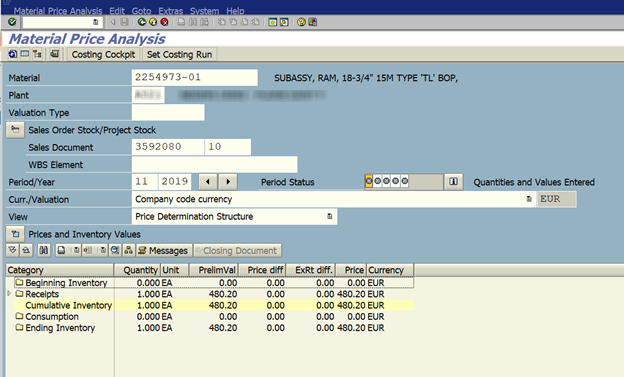

Inventory Books have the real value of the planned inventory, can be reviewed via transaction CKM3N as shown in Figure 27.

Figure 27: Inventory Books Review

Benefits

- More accurate manufacturing cost

- Potentially less variances

- No change in the Gross Margin

- Visibility of actual cost across plant transfers

What Does This Mean for SAPinsiders?

Information mentioned in this article is applicable to small-, medium- and large-sized organizations. Based on these guidelines, SAPinsiders should:

- Identify your product fit on volume/variety. On the shelf products typically fall into make-to-stock category so it is straight forward to manage the cost of product using standard cost on material master. On the other hand products having manufacturing processes including either batch production, job shop production types fall into make-to-order category Where managing customer requirements is a very common scenario so you should adopt the process which can capture the costs of planned vs unplanned customer changes to post accurate inventory value on the books and improve transparency.

- Know how to manage planned changes in make-to-order manufacturing. Standard SAP planning strategies provide insight end methodology with configurable options to manage cost effectively on manufacturing and procurement processes. Organizations may explore the best practices mentioned in this article to minimize the risk during variance calculations and improve efficiency during month end closing processes, Implementations of make to order planning strategy is a project so include all your key stakeholders from manufacturing, finance and logistics teams, involve change management so invest time in user training.

- Configure system for better cost management and avoid workarounds. Managing costs in manufacturing processes is not a straight forward and in most of the organizations struggle to differentiate the variances so the planners and cost accountants should understand the standard, planned, target costs and involve IT to configure the SAP planning strategy to suit the reality and avoid manual workarounds during variance and settlement calculations on production orders, adopting appropriate configurations improve visibility, accuracy allow improved cost versus margin analysis.